Disconnect between value creation and capture

The venture capital industry creates value that far outweighs the dollars allocated to it. But ten year returns to investors haven’t reflected that fact.

Innovation presents opportunities to solve customer problems more effectively and efficiently. But creating solutions that don’t yet exist involves a high degree of uncertainty. Usually, you need to spend a considerable amount of time and money before you know your efforts are going to pan out. That’s where risk capital comes into play; private investors invest money with the hopes of earning outsized returns to account for the level of risk they’re taking.

Source: PricewaterhouseCoopers/National Venture Capital Association

Venture Capital is one of the most important sources of risk capital around. Limited Partners (LPs) commit money to venture capital funds managed by General Partners (GPs). In aggregate, US GPs put roughly $25 billion to work every year. That might sound like a lot of money, but it’s less than 0.2% of US GDP.

Yet that 0.2% has been key in creating companies that account for 21% of the US GDP, and over 11% of private sector jobs (read the report). A tiny fraction of GDP invested by venture firms every year has been instrumental in creating more than one-fifth of the value in our economy.

Of course, venture financing isn’t the only funding source most of these successful companies have used to get where they are. After getting their venture dollars, many have taken in money from banks, mezzanine funds, and public offerings. But for most of these companies, it was venture financing that made them big; by the time they qualify for later-stage funding events, their valuations are often huge.

Clearly, venture capital investing results in tremendous asset value creation, particularly when compared to the dollar inputs.

But where is the payback for investors?

The problem is that LPs are capturing very little of the value created. Over the past ten years, the average venture LP would have generated better returns investing in an index fund such as the S&P 500. Ten year returns for early stage venture were 3.9% as of 2013, while returns for the S&P 500 for the same period were 8%. And that’s before adjusting for risk, which makes venture returns appear even more lackluster.

I have heard two common objections to this line of reasoning, and they go something like this (followed by my rebuttals):

“If you look at the past 25 years, the numbers look much better for venture. This has just been a bad 10 years.”

Ten years is a pretty long time. And we’re talking about how venture tracks against a broad market index; it’s not like we’re expecting absolute returns to be awesome. Going back 25 years lumps in the dot-com boom, and I’m not convinced there’s any real likelihood we’re going to see another valuation and liquidity explosion like that again. Rather, I see evidence of fundamental structural changes in the venture industry that are causing these poor returns.

“It’s all about the top performing firms; you need to focus on the incredible returns they make.”

If we’re talking about what a typical LP should expect, averages are what matter. Perhaps if you’re an existing investor in one of the old-school top-tier venture firms, this argument is meaningful for you. Frankly, it’s probably the opposite for most LPs; they don’t have a snowball’s chance in hell of getting into one of those top funds. Even then, you might want to think twice; it’s not clear historical performance for those funds is a good predictor of future outcomes.

The Kauffman Foundation (a non-profit dedicated to education and entrepreneurship) wrote a scathing report in 2012 entitled, “We have met the enemy… and he is us.” The foundation is a large and experienced venture investor, with (at the time) $249 million of their total $1.83 billion investments allocated to 100 different venture firms. Here are a few choice things they had to say:

- 62 of 100 firms failed to exceed returns available from the public markets, after accounting for fees and carry

- 69 out of 100 did not achieve sufficient returns to justify investment

- venture fund GPs have little actual money at risk in their own funds: an average of 1%

- the “2 and 20” model means that GPs are assured of high levels of personal income, regardless of the performance of their investments

- venture funds were taking on average far more than 10 years to return liquidity (when they did)

In summary, they said: “Returns data is very clear: it doesn’t make sense to invest in anything but a tiny group of ten or twenty top-performing VC funds.”

Market forces impacting venture

A combination of structural factors, historical trends, and market dynamics are creating tremendous pressure on the venture capital industry.

The “2 and 20” structure

The vast majority of venture firms work on some (minor) variation of the 2 and 20 structure whereby the fund managers get 2% per year of the committed funds for salaries and operating expenses (“management fee”), as well as 20% of the net value created (“carry”). Since most funds last ten years, that means 20% of investment dollars (2% times 10 years) never even reach the portfolio companies. Sometimes the annual percentage amount drops after the active investing period. Still, net of higher annual percentages (2.5% is fairly common) and long investing periods, the reality is that somewhere around 20% of investor dollars are taken off the top.

There is nothing intrinsically wrong, or even irrational, about the 2 and 20 model; it’s fairly common in other segments of the finance industry such as hedge funds and traditional private equity (although read here and here to see how those industries may be changing). There’s also nothing wrong with investors making multi-million dollar salaries. But in the face of such poor venture returns, it is hard to justify the current economic structure.

Ironically, it’s the 2 and 20 structure that is in part responsible for a chain of events that have contributed to the decline in venture returns over the years. As time goes on, it seems that the fundamental economics of the venture model are putting the entire industry at risk.

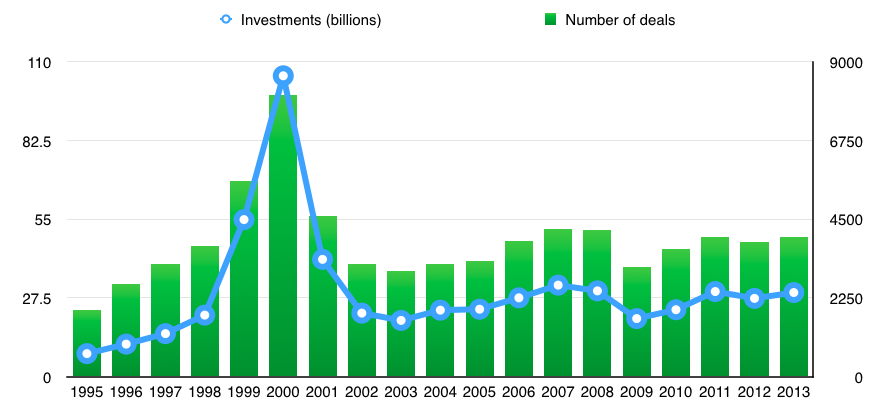

A rising tide

The dot-com era was an extraordinary period of value creation, and many savvy venture capitalists made the most of it. As the IPO market exploded, so did the returns for the venture funds who were smart enough to be in the right deals at the right time.

During the five-year period between 1996 and 2000, the US markets saw 1,227 venture backed IPOs. And the VCs were cleaning up, with a median ownership stake of 40%. Perhaps more importantly, IPO returns averaged a stunning 88% during 1999 and 2000 (read the study).

Opening the floodgates

With venture funds practically minting money, the financing floodgates opened. Billions of dollars poured into venture capital funds, and many new funds formed. By the peak of the bubble in the year 2000, there were 1,022 active US venture capital firms.

And it wasn’t just the number of firms that ballooned; the average size also grew rapidly. And the size of the firms grew much faster than the number of GPs. According to data from the NCVA, average capital per principal rose from about $3 million in 1980 to roughly $30 million by the late 2000s–roughly 10x growth.

Why did dollars managed per partner grow so much? It’s almost certainly due to the incentives associated with the 2 and 20 structure. The more dollars per partner, the more management fee, and potentially, the more carry. Increasing the size of a fund pro rata with the number of partners wouldn’t be in their interests. And if the LPs were willing to invest more money on those terms, it’s only natural that the GPs were happy to oblige.

The requirement for massive exits

Deborah Gage wrote in her 2012 Wall Street Journal article that the common rule of thumb for venture outcomes is 30-40% completely fail, another 30-40% return the original investment, and 10-20% produce substantial returns. However, her article then points out that research into over 2,000 venture backed companies by Shikhar Ghosh suggest numbers that are somewhat more stark:

- 30-40% return nothing to investors

- 75% don’t return investor capital

- 95% don’t achieve a specific growth rate or break even date

That suggests that it’s closer to 1 deal in 20 that returns a meaningful amount of money, and another 3 in 20 that return capital.

Let’s do a little bit of venture math

What sort of return would the one big winner require to make the fund? First, the fund and it’s goals:

- $125 million fund that makes 20 investments

- Typical 2 and 20 structure, with 2% average over 10 year fund lifespan

- Due to follow-on investments in the good deals that, each accounts for 10% of fund, rather than the expected 5%

- The fund needs to return at least 2x overall to investors to ensure they can raise another fund

- With 20% carry, they need to return 2.5x, or $312.5 million to hit their goal

Investment dollars, and expected outcomes:

- They’re investing $100 million net of 20% management fee

- 3 so-so deals return an average of 2x each

- 8 deals return an average of 1x each

- 8 deals are a total wipeout

Here’s how the math works out:

- The goal is 2.5 times $125 million, or $312.5 million

- $40 million into 8 deals generates $0

- $40 million into 8 deals generates $40 million

- $20 million into 3 deals generates $40 million

Without the big winner, they’ve returned $80 million out of a target of $312.5 million, which is $232 million short.

So, what return does their “fund-making” investment need to achieve? With $10 million invested in the big winner, they need a $232 million (23x) return to make their target minimum. More likely, they’re actually targeting a 3x overall fund return, which would imply that they need more than a 43x return in that one deal to make their numbers.

Wow. And to put that in perspective, those returns imply much higher enterprise valuations. Assuming the VCs own a third of the company at the time of liquidity (and ignoring a presumed 1x liquidation preference), we’re talking about an enterprise valuation of $696 million for that one company to achieve the overall 2x return on their fund.

That’s the sort of math that forces most venture capitalists to seek massive exits to make their fund economics make sense.

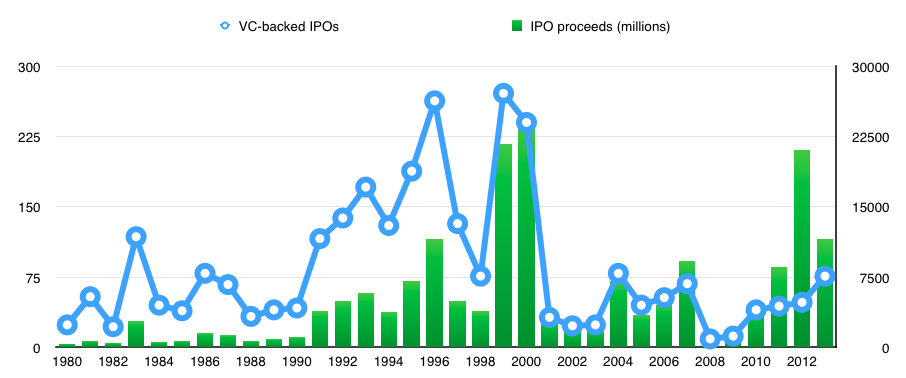

A weak IPO market

During the massive growth of the venture industry in the 1990s, funds relied in large part on the booming IPO market to achieve these extraordinary liquidity multiples. The returns for some funds of that era are truly astonishing. But the turn of the century brought a whole new economic reality to the venture market. The IPO market dried up extremely quickly, and has only slowly begun to recover over the past few years.

Even with recent improvements, however, the IPO market is nothing like what it was during the boom times, and likely never will be again. The number of issuances is down, and the economics for the investors are far different than they were previously. No more 40% stakes in the companies at IPO, or reasonable expectations for 88% returns from the IPO.

Rather suddenly, venture capitalists had all but lost their most important liquidity generation tool.

Venture’s new reality

The result is larger funds, higher valuations, and later stage investments, which in turn require even bigger liquidity multiples. Without a highly active IPO market, that’s a significant challenge.

More capital per partner means bigger investments

When a fund grows at a rate three times faster than partner growth, it’s not as if each partner can source three time as many quality deals, and perform diligence three times as efficiently. An obvious solution is to put more money to work in each deal, rather than simply increasing the overall number of deals.

That probably explains the trend towards larger deal sizes, and in particular more “loading up” on existing investments in the form of follow-on financings. Peter Delevett’s article in the San Jose Mercury News quotes entrepreneur Tony Jamous, who says, “There’s so much money right now in the market that it’s my challenge to actually keep it a small round.”

Revenue generating is the new seed stage

Just because GPs are investing more dollars in each deal doesn’t necessarily mean that they’re acquiring more of the company. Venture investing is not about making control investments; it’s about backing a team. Given the prospect of follow-on rounds, it simply doesn’t make sense to take too much of a company in early venture rounds; otherwise, you’re setting yourself up for a recapitalization when the entrepreneurs find themselves squeezed into a small corner of the cap table.

The obvious way to put more money into a company, while maintaining a suitable portion of the cap table, is to invest in companies that are worth more. That, in turn, implies investing in companies that have reduced risk by making more progress.

That’s why so many venture firms are investing later stage, where risk is lower, and valuations are justifiably higher. Later stage investments are also easier to diligence because there’s more of a track record. Ernst and Young’s Turning the Corner report from 2013 said it pretty succinctly: “VC funds are adjusting their investing strategies, preferring to invest in companies that are generating revenue and focusing less on product development, pre-revenue businesses.”

And Paul Graham, founder of Y Combinator, is clearly seeing it in the market, too, referring to “…what used to be the series A stage before series As turned into de facto series B rounds.”

Venture investors are investing later in the risk curve, meaning they have mostly vacated what used to be seed stage, and seed stage investments now are more similar to what Series A investments used to be. That in turn pushes Series B and later rounds further along the risk continuum.

Bigger investments often mean higher valuations

As traditional venture capitalists move away from true seed stage investing, they’re beginning to clump at the later stages, with more investment dollars targeting a relatively stable supply of viable startup investments. That stable supply and increased demand tend to push valuations higher.

That’s further exacerbated by the generally high levels of LP investments over the past decade. Despite relatively poor returns, Limited Partners continue to pour money into the industry, albeit with what appears to be an increasing emphasis on a smaller set of funds with the best track records. The excess capital active in the later stages of the venture market have resulted in a war for tech companies with demonstrable traction, resulting in even further valuation inflation.

The venture valuation bubble

For a number of years, I’ve struggled to reconcile the evidence of frothy venture valuations with the inability of amazing entrepreneurs to acquire funding. I suspect the best explanation is that both are true; seed stage investments are irrationally hard to achieve, while mid-stage deals are overly competitive.

Revisiting Paul Graham’s June 2013 essay on Startup Investing Trends (referenced earlier):

“Right now, VCs often knowingly invest too much money at the series A stage. They do it because they feel they need to get a big chunk of each series A company to compensate for the opportunity cost of the board seat it consumes. Which means when there is a lot of competition for a deal, the number that moves is the valuation (and thus amount invested) rather than the percentage of the company being sold. Which means, especially in the case of more promising startups, that series A investors often make companies take more money than they want.”

There is tremendous pressure in the venture industry to invest more money, at higher valuations, in more mature companies.

Higher investment valuations require higher exit valuations

We have already discussed the economic imperative for venture firms to seek massive exits. What happens when those already lofty multiples are rebased on a significantly higher initial investment valuation? It simply means that the size of the liquidity events required to achieve success are all that much larger.

The entrepreneurs are feeling it, too. Peter Delevett’s article in the San Jose Mercury News goes on to quote venture investor Craig Hanson: “In other words, too much money now makes it harder for the VC firms and entrepreneurs to strike it rich later.”

Swinging for the fences

IPOs are typically the best way for venture funds to achieve massive liquidity, but they remain elusive targets. Even when the IPO markets are working, there is a finite supply of companies that are suited to an IPO. Bruce Booth wrote a 2012 piece about venture capital, saying “… it’s not the lower frequency of winners in general, but the lower frequency of outsized winners, that has dampened returns in the asset class.”

This is creating a dilemma for venture capitalists. Their strongest economic imperative is to maximize the capital under management per partner. Success for most is more about raising and layering funds than generating income through carry. That’s not to say that they don’t hope for massive payouts from carry, but the changes in the market have made it increasingly difficult to achieve that.

Here’s a colorful way to think of it: the home run king is under pressure to beat a field of top-notch batters. But this season, they moved the fence out 100 yards farther than before. A miss is as good as a mile; the only thing he can do is swing with all of his heart.

For many venture funds, their singular goal is to invest in those very few mega deals that deliver crushing returns. Anything less simply won’t move the needle.

The future of venture capital

While venture capital is certainly here to stay, it’s clearly an industry in flux. Investors and fund managers are beginning to adapt. Meanwhile, exciting new models are beginning to emerge.

Venture capital is here to stay

Venture capital is by no means going away. It’s an important, multi-billion dollar industry, filled with talented, intelligent, and often charismatic people. Many of them are experienced entrepreneurs accustomed to dealing with change and uncertainty. The likelihood is that they’ll figure out a way to thrive, and that in turn implies that they will be able to continue to make money for their investors.

There are also some trends that will likely change some of the industry dynamics for the better. Those include:

- While the past 10 years have been bitter for many venture capitalists, there is recent evidence of an upward trend.

- The overhang in LP capital commitments is mostly worked out, and there is some evidence capital inflows are moderating to a more sustainable pace.

- The NVCA estimates there were 462 active US venture firms, down from 1,022 in the bubble of 2000; that is likely a reduction to quality, and a more appropriate overall market size.

- There is evidence that the IPO markets are reviving, improving potential liquidity opportunities.

- The underlying value created by many venture investments is real in a way that probably wasn’t true to the same extent during the dot-com era.

- There is evidence that LPs are focusing more on track records of the actual investing partners, which is probably a more efficient rubric for selection.

- There is some evidence that GPs are willing and interested to engage in a dialog about how to evolve the economics and structure of their funds.

But it is an industry in flux

I think Wade Brooks sums it up nicely in his TechCrunch article when he says, “early stage venture investing does not occur in an efficient market.” Returns to investors over the past ten years have been inadequate, and the Limited Partners are beginning to change their behavior. And the fundamental economics will not be tenable for many funds; I expect continued fallout, and further winnowing of funds.

New models emerging

Perhaps most importantly, there are new investment models emerging. These may be hybrid models where venture capitalists add value in new ways, such as Andreessen Horowitz. Or, in the case of 500 Startups, revolutions in the ways that professional investors select and invest in companies. In some cases, it may be fundamentally different approaches to investing, such as crowdfunding. Meanwhile, we can’t forget Angel investing, which offers the chance to capture enormous value, albeit with certain caveats.

And, of course, there’s the new approach that we’re taking here at Founder Equity, which we believe offers the chance to create more value, more quickly, and with reduced risk. We look forward to sharing more with you as we continue our journey.